Many people try to get rich by emulating multi-billionaire Warren Buffett’s investment strategy. There’s great, though they miss (or choose to ignore) an important ingredient – one reason Buffett is so rich is because he is also infamously frugal.

There are numerous examples of Buffett’s frugality. For example, when his first child was born, Buffett converted a dresser drawer into a bassinet . For his second child, he borrowed a crib. He drove a Volkswagen until his wife upgraded him to a Cadillac (which she felt was better for his image). Buffett still lives in the Omaha, Nebraska, in the house he bought for $31,500 more than 50 years ago. You get the drift…

Buffett manages his money and wealth on the principle that small sums compound. Every penny not spent today means a lot more money to invest, or use, in the future. In the book The Millionaire Next Door, Stanley and Danko also found some interesting truths about many millionaire households that they profiled in America – most of the millionaire households that they profiled did not have extravagant lifestyles and luxury items like branded watches, suits, cars etc.). They accumulate so much wealth precisely because they live below their means.

T. Harv Eker summarizes it with these wise words: “The habit of managing your money is more important than the amount.” And this is one of the 17 factors that differentiates rich people from poor people.

How can you systematically manage your money better? Well, in his book Secrets Of The Millionaire Mind, Eker shares a simple method that anyone could use.

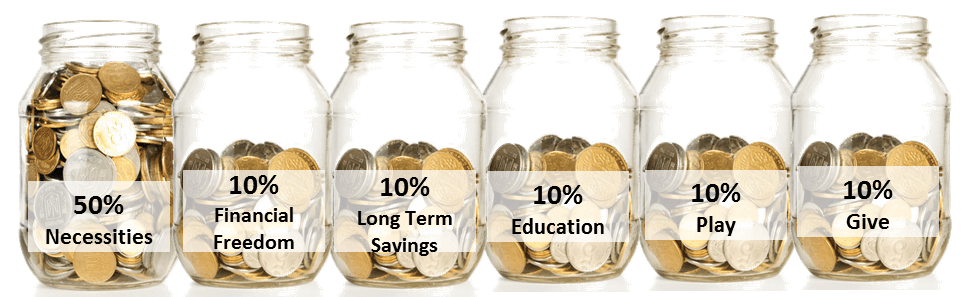

THE 6 JARS CONCEPT FOR WEALTH MANAGEMENT

The idea of this system is simple: separate your income into 6 different accounts for specific purposes. You can also use physical jars, envelopes etc. and label them accordingly. The most important thing is to consistently deposit into these jars / accounts as follows:

Necessities (50%):

Half of your income goes toward real necessities (N) like food, mortgage payments, bills, gas, oil, insurance, etc. If you can’t cover all your necessities with 50% of your income, you need to do one (or both) of these things:

1. Simplify your life – figure out how you can spend less

2. Earn more – figure out how you can earn more

Financial Freedom Account (10%):

10% of your income goes into your Financial Freedom (FF) jar. The money in this jar can only be used for investments (with returns or profits). This jar is used for building wealth for your future financial freedom. You must never spend this money.

Long Term Savings (10%):

10% of your income goes into the jar called Long Term Savings (LTS) for Spending. The objective of of this jar is to save money for future expenses (e.g. a new car, a vacation, a new couch, gifts, repaying debts…).

Education (10%):

Successful people constantly invest in and grow themselves. Hence, 10% of your income goes into the Education (E) jar. The more knowledge and skills you acquire, the greater your earning capacity. And the more you earn, the more you need to learn (how to manage your additional wealth, how to bring your income to the next level etc.). Use the money from this jar for personal or professional development (e.g. books, courses, seminars).

Play (10%):

10% of your income goes into the Play (P) jar. It’s important to occasionally indulge yourself with a nice massage, some new clothes, a fancy dinner… To avoid over-spending or under-spending, make sure you use up the money from this jar at least every few months. This allows you to spend without guilt, and to also gradually improve your standard of living as your income increases.

Give (10%):

10% of your income goes into the Give (G) jar. However poor your circumstances may be, there will always be someone who is in an even more dire state. Besides the feel-good factor of helping others, giving away part of your income also helps you to sub-consciously develop the wealth-mentality that you have more than enough to give away.

Financial Freedom Jar:

Finally, create a Financial Freedom Jar and deposit something into it daily, however small. The idea is to keep financial management top-of-mind, and a daily commitment made towards your financial freedom.

Once again, to summarize, here are the 6 jars concept:

GETTING STARTED

Obviously, these numbers are just guidelines. Depending on your financial circumstances, you may need to adjust the percentages slightly. Even if you are currently in debt, you can start by managing each borrowed dollar well. In fact, if you are heavily in debt, there’s all the more reason to start implementing this system.

Here are 3 simple steps to get started:

1. Know your percentages. You can’t manage your money without knowing how much you are earning and spending. You can start by calculating your current monthly income and the amount to be put into each of the 6 jars. Then, track how much money you spend daily. Just by becoming aware of your spending patterns is already a first step in the right direction.

2. Shift your mindset. Understand that money management isn’t about restricting your freedom; it is to create eventual financial freedom. Several years from now, you can be happily retired while your friends (who are enjoying the “good life” now) are still slogging away to pay for their expensive lifestyle. Constantly remind yourself out loud “I am an excellent money manager!”

3. Don’t entertain any excuses. It’s easy to say “I’ll do it tomorrow”, or “I don’t have time for it”. The big question to ask yourself is – how badly do you want to be rich and financially free? If you are serious about your financial goals, then no excuses should be permitted. Start NOW and stick to your plan.

The real insight lives across books

Connect insight and ideas for a full picture on Personal Wealth and Money

APPLYING THE 6 JAR CONCEPT TO YOUR BUSINESS

If you’re running your own business and struggling to pay the bills each month, it’s time to start turning things around. Read up more on how you can apply a similar concept to transform your business finances and take Profit First.

FEELING STUCK?

What if you’ve tried to apply the 6 Jar concept, but found yourself getting stuck? Perhaps you couldn’t make the sums work (“there’s no way I can squeeze my expenses into 50% of my salary!”), or perhaps you kept slipping back into your old habits and can’t find the discipline to stick to the plan….

Don’t worry, it happens to the best of us. Acknowledging that you’re stuck already puts you 2 steps ahead of the pack. Here are 2 things you can do:

• If you are determined to have a breakthrough – be it in your finances or other aspects of your life – we recommend that you get yourself a coach – someone who can help you find the way, and hold you accountable to deliver the results you want. Now, this requires that you’re committed to succeed; and from our experience, most people aren’t. If you’re ready to do what it takes for results, then click on this link. We have a special arrangement with T-Harv Eker’s team, meant for graduates of his program. We are making it available to you. So go ahead and find out more here. You can thank us later.

• Prefer a DIY approach at this point? Read our free Secrets of the Millionaire Mind summary, or buy the full text, graphic and audio book summaries.

Click here to download Secrets of the Millionaire Mind book summary and infographic